This year, governance has become one of the hottest topics in decentralized finance (DeFi) thanks to the issuance of a swathe of governance tokens at some of DeFi's biggest projects. These include lending platforms and decentralized exchanges (DEXs) Maker, Compound, Aave, and Uniswap, which have seen their market caps soar since the spring.

A governance token gives holders voting rights over proposed revisions to smart contracts at issuing protocols, allowing them to have their voices heard when it comes to making changes to how that protocol operates. Some governance token holders also benefit from a share of protocol fees, trading fees and other rewards, particularly those issued by DEXs like Uniswap for depositing into its liquidity pools.

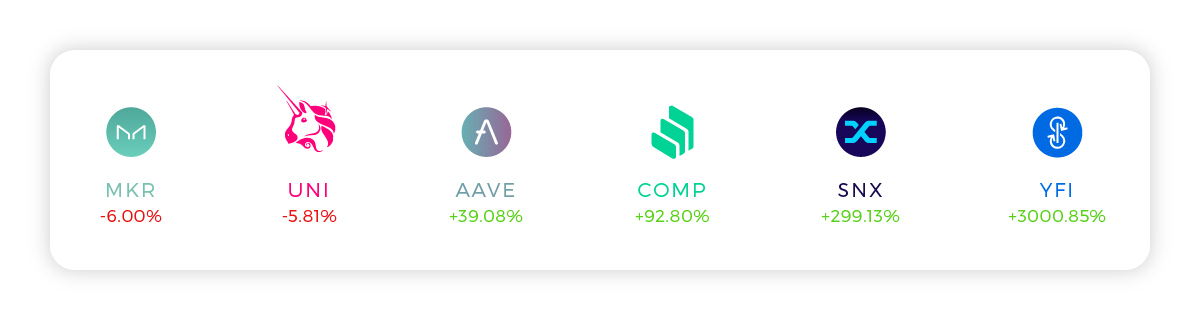

As has been regularly stated by issuers, though, governance tokens have no intrinsic value: they are not utility tokens. Nonetheless, they are highly attractive to many DeFi users, which has supported a steep rise in the price of many of these tokens. This is not least the case for YFI, the governance token of yearn.finance, which has risen from $790 at launch in July 2020 to close to $25,000 by December 2020, representing a market cap of $740 million.

Source: coingecko.com/en/defi

An important function of DeFi

For many in the crypto space, a governance token is a key functionality of a DeFi protocol that allows decentralization to work. A good example would be Maker DAO, issuer of the dollar-pegged stablecoin DAI, which in March this year finalized its transition to complete community governance.

In the wake of COVID-19, cryptocurrency values plunged, sending shock waves through the DeFi ecosystem and causing numerous vaults to be automatically liquidated. For DAI, though, it was a particular problem as the huge plunge meant its value dropped below parity with the US dollar: it's raison d'être.

As such, the Maker community called for the introduction of a voting process linked to the protocol's token, MKR, that could allow changes to be made to the smart contract that governs it. This includes required levels of collateral, stability fees for opening Maker Vaults and, more recently, the debt ceiling for ETH. All of these measures help to keep the price and total supply of DAI stable.

DeFi democracy in action

While the above could have been achieved without the input of Maker DAO users, this approach is in line with the decentralization of finance that the system hopes to achieve. As we have covered previously on our blog, the principles of DeFi centre around financial democracy: the ability for all users to be able to participate and have a say in a monetary system that works in favor of the majority.

Along with Maker, other success stories include the $619 million market cap derivatives liquidity protocol Synthetix, which after governing by rough consensus since its founding in 2018, launched this year three DAOs that will each manage separate parts of the protocol. While each will effectively be controlled by a group of lead developers, this is an indication of the direction of DeFi.

Uniswap's governance token has also recently allowed its users to vote on whether liquidity mining would continue on the platform, while a voting majority of Curve Finance token holders voted to distribute nearly $3 million in accrued fees among themselves. For some, all of this is leading toward a future in which we could see organizations, perhaps not just in DeFi, governed entirely based on token ownership.

Where does value come from?

Governance tokens have soared in value over the course of this year. As of today, the six largest DeFi governance tokens (AAVE, YFI, UNI, COMP, SNX and MKR) have a combined market cap of $4.1 billion - not too far behind Bitcoin Cash's $4.8 billion. So where did all this value come from?

Part of the answer lies in the interplay between liquidity mining, lending and staking. Compound, for example, is considered a pioneer in the governance space because it rewards users with COMP, which encourages them to lend and borrow to gain more tokens and effectively insure themselves against ever defaulting on a loan. In this way, COMP creates its own demand.

Then, of course, there is old-fashioned speculation. Like so much in both traditional money markets and the crypto space, interest in governance tokens is driven by a hope that the tokens and the protocols behind them will grow as valuable items. The decentralization of finance is just about the hottest trend in crypto right now, if not the broader money world, and people are keen to be part of, and potentially cash-in on, the ability to influence how these projects are run.

Source: coingecko.com/en/defi

Is governance too centralized?

However, while the user governance aspect of DeFi is one of the many appealing solutions that crypto offers compared to the closed world of traditional finance, it is not without problems. Among these are DeFi protocols that have many pre-mined tokens, typically held by founders. Close to 50% of COMP tokens, for example, were distributed to its founders, team, and shareholders, giving this group huge sway over the operation of the protocol and its liquidity pools.

In these instances, where a significant portion of the total supply of a token rests with a founder, governance is effectively centralized, which is not what DeFi aims for. Moreover, the functioning of the protocol can also be put at risk when founders sell a large part of their tokens in one go. SushiSwap's creator Chef Nomi, for example, sold approximately $13 million worth of SUSHI tokens from the developer's fund last September, inciting a plunge in the token's value and a crisis in confidence. Chef Nomi ultimately returned the funds to the treasury, but it caused considerable damage to SushiSwap's image.

As time goes on and the governance power of these DeFi tokens increases (as speculators hope), they may also become vulnerable to "hostile takeovers" where an investor or investors buy up huge quantities of tokens in order to influence the direction of projects. The effect of this is well documented in traditional finance, where aggressive hedge funds typically vie for a controlling stake of a company or fund and then pump its operations before draining profits and exiting.

The evolution of governance

These problems have been met with responses from some DeFi projects and platforms that are seeking to find solutions to limit the negative impacts of the governance token mechanism. In the case of a large dump of tokens, for example, DeFi lender Aave has implemented a "Safety Module" where users can lock their governance tokens away for rewards, and which can be drawn on during "shortfall events."

Moreover, as DeFi protocols grow and require further development, it is likely that founders will sell down their holdings in order to fund that work, gradually reducing their ownership in those projects. Selling their stakes in this way will ultimately increase the value of the tokens and the protocol, which means their interests are strongly aligned with those of all users and governance token holders.

The question of value is an important one as well, with many asking how tokens like YFI can hold on to such high values in an ecosystem where these tokens have no intrinsic value. That same argument, however, was once made about Bitcoin, and we all know how that turned out.

Do you want to earn market-leading interest rates on your digital assets? Sign up for a YIELD App account today!

DISCLAIMER: The content of this article does not constitute financial advice and is for informational purposes only. The price of digital assets can go down as well as up, and you may lose all of your capital. Investors should consult a professional advisor before making any investment decisions.